Nic Dunn, CEO, Charle Agency

Nic Dunn, CEO, Charle Agency

Best BNPL Apps for Shopify UK: Comparison Table

| Rank | App | Payment Model | Best For | Merchant Fees |

|---|---|---|---|---|

| 1 | Klarna | Pay in 3, Pay Later, Financing | Fashion and lifestyle brands | From 2.49% + variable |

| 2 | ClearPay | Pay in 4 interest-free | Gen Z and millennial shoppers | Flat % per transaction |

| 3 | Shop Pay Installments | Pay in 4 or monthly | All Shopify merchants | Included with Shopify Payments |

| 4 | PayPal Pay Later | Pay in 3 | Brands with PayPal checkout | Standard PayPal rates |

| 5 | Laybuy | Pay in 6 weekly | Fashion and retail | Percentage per transaction |

| 6 | Splitit | Use existing credit card | High-ticket items | Per-transaction fee |

| 7 | Affirm | Monthly instalments up to 60 months | High-value purchases | Merchant fee varies |

| 8 | Sezzle | Pay in 4 interest-free | Budget-conscious shoppers | 6% + £0.30 per transaction |

| 9 | Scalapay | Pay in 3 or 4 | European-focused brands | Percentage per transaction |

| 10 | DivideBuy | Interest-free and interest-bearing | Furniture, electronics, high-value | Variable based on terms |

10 Best Buy Now Pay Later Apps for Shopify UK (2026)

The following apps represent the best BNPL solutions currently available for Shopify merchants in the UK. Each has been selected based on real-world integration experience, conversion impact, customer reach, and merchant fee structures. Whether you are looking for maximum market coverage or a niche solution tailored to your specific product category, one of these providers will meet your needs.

1. Klarna

- Best For: Fashion and lifestyle Shopify stores

- Pricing: From 2.49% + variable per transaction

- Payment Options: Pay in 3, Pay Later 30 days, monthly financing

- Availability: UK, Europe, USA, Australia

Klarna dominates the UK BNPL market with unmatched brand recognition and market penetration. The platform processes over £4 billion in annual spending across the UK alone and counts household names like ASOS, H&M, Samsung, and JD Sports among its merchant partners. The Shopify integration is straightforward via the Klarna app, and the platform offers sophisticated on-site messaging widgets that appear contextually during the customer shopping journey, encouraging larger basket sizes before checkout.

What sets Klarna apart is the flexibility of its payment options. Unlike competitors offering fixed instalments, Klarna presents customers with Pay in 3, Pay Later (full amount in 30 days), or monthly financing options, allowing each customer to select the payment method that suits their cash flow. The platform's real-time decisioning means most approvals happen instantly, and the redirect checkout experience has been refined over years to minimise friction.

We have integrated Klarna across multiple Shopify Plus builds and the conversion uplift is consistently strong. Customers respond particularly well to the brand trust that Klarna carries, especially in fashion and lifestyle verticals. The merchant fee structure is competitive at the lower end, and Klarna's underwriting means you have lower chargeback rates compared to some alternatives.

Key features: On-site messaging, Pay in 3 and later options, integrated decisioning, native Shopify Payments integration, comprehensive merchant dashboard with analytics, fraud protection included, next-day settlement.

Why choose them: If you operate a fashion or lifestyle brand targeting UK customers, Klarna is the default choice. The brand recognition alone drives conversion, and the diversified payment options give customers flexibility. The integration is native to Shopify, meaning minimal technical overhead.

2. ClearPay

- Best For: Gen Z and millennial-focused brands

- Pricing: Flat percentage per transaction

- Payment Options: Pay in 4 interest-free fortnightly instalments

- Availability: UK, Australia, New Zealand, USA (as Afterpay), Canada

ClearPay is the UK brand of Afterpay, owned by Block Inc. (formerly Square). The platform has cultivated a reputation as the BNPL provider for younger generations, with particularly strong appeal among Gen Z and millennial shoppers. Major retailers like Boohoo, JD Sports, and Urban Outfitters rely on ClearPay, and the platform's integrated shopping discovery feature helps merchants reach new customers beyond their immediate audience.

The ClearPay model is refreshingly simple. Customers pay in 4 equal fortnightly instalments, entirely interest-free. If a payment is missed, a late fee applies, but there is no interest charged. The straightforward nature of this offering appeals to younger customers who appreciate the simplicity compared to Klarna's multiple options. ClearPay's underwriting is lenient, meaning approval rates are generally high, which boosts conversion metrics for merchants.

The platform's shopping discovery network is particularly valuable for brands wanting to reach new audiences. ClearPay customers browse merchants on the platform itself, creating a source of incremental traffic beyond your own marketing efforts. This makes ClearPay especially valuable for growing brands that need both conversion uplifts from existing traffic and access to new customer cohorts.

Key features: Simple pay-in-4 model, shopping discovery network, integrated messaging, merchant dashboard with forecasting, fraud protection, flexible refund handling, next-day settlement.

Why choose them: If your target audience is Gen Z or millennials, ClearPay delivers both conversion benefits and customer discovery. The simplicity of the pay-in-4 model means less customer confusion at checkout compared to platforms offering multiple payment options. The shopping discovery feature provides a direct channel to potential new customers.

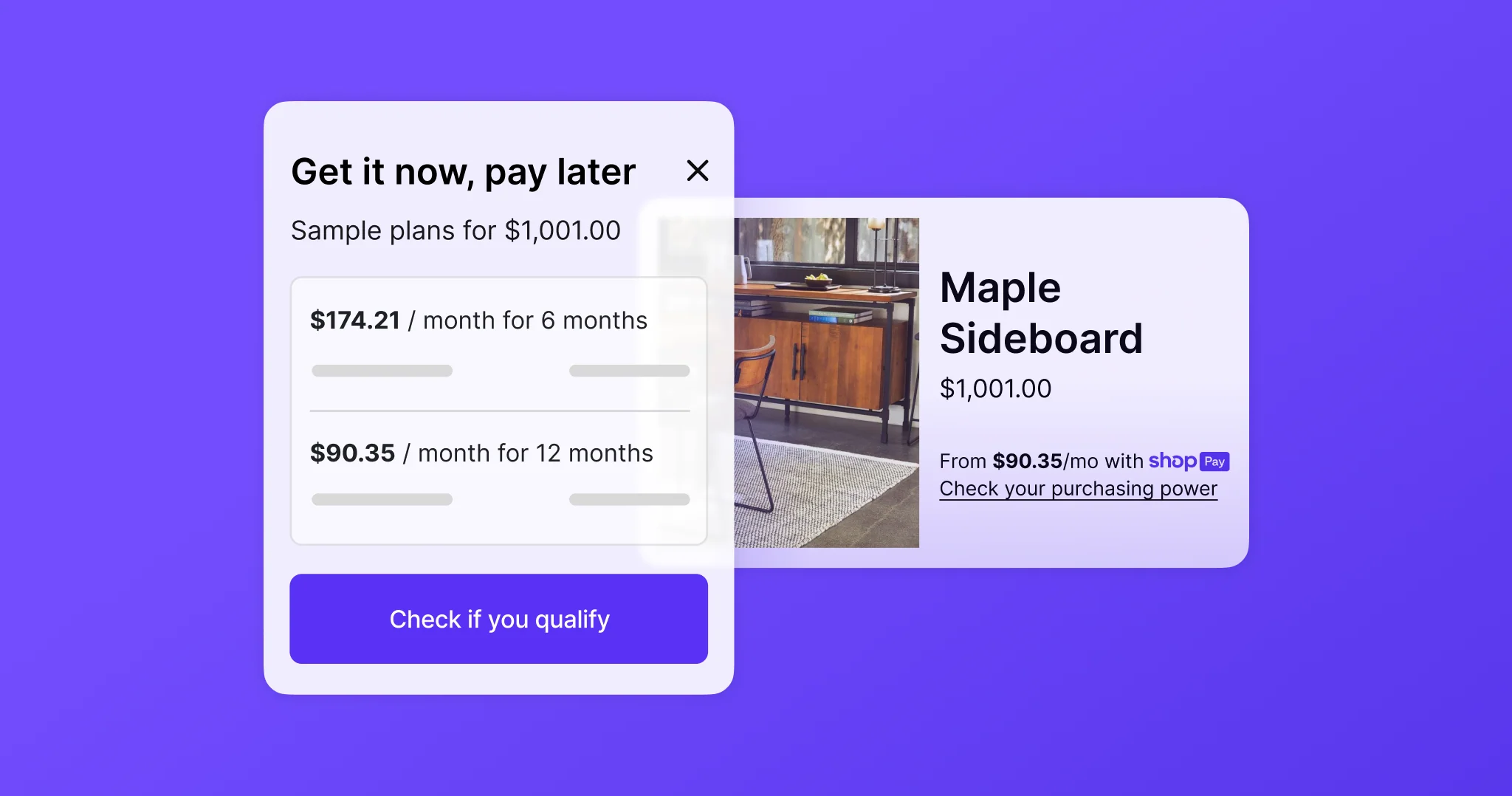

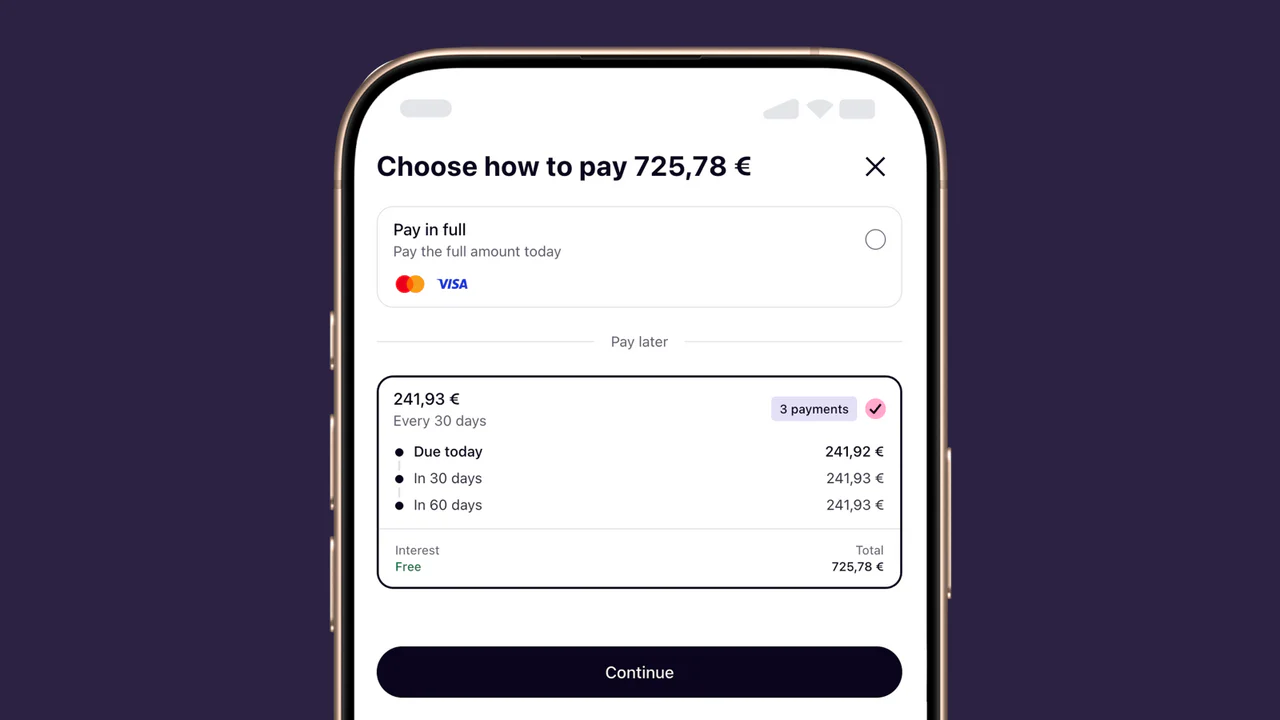

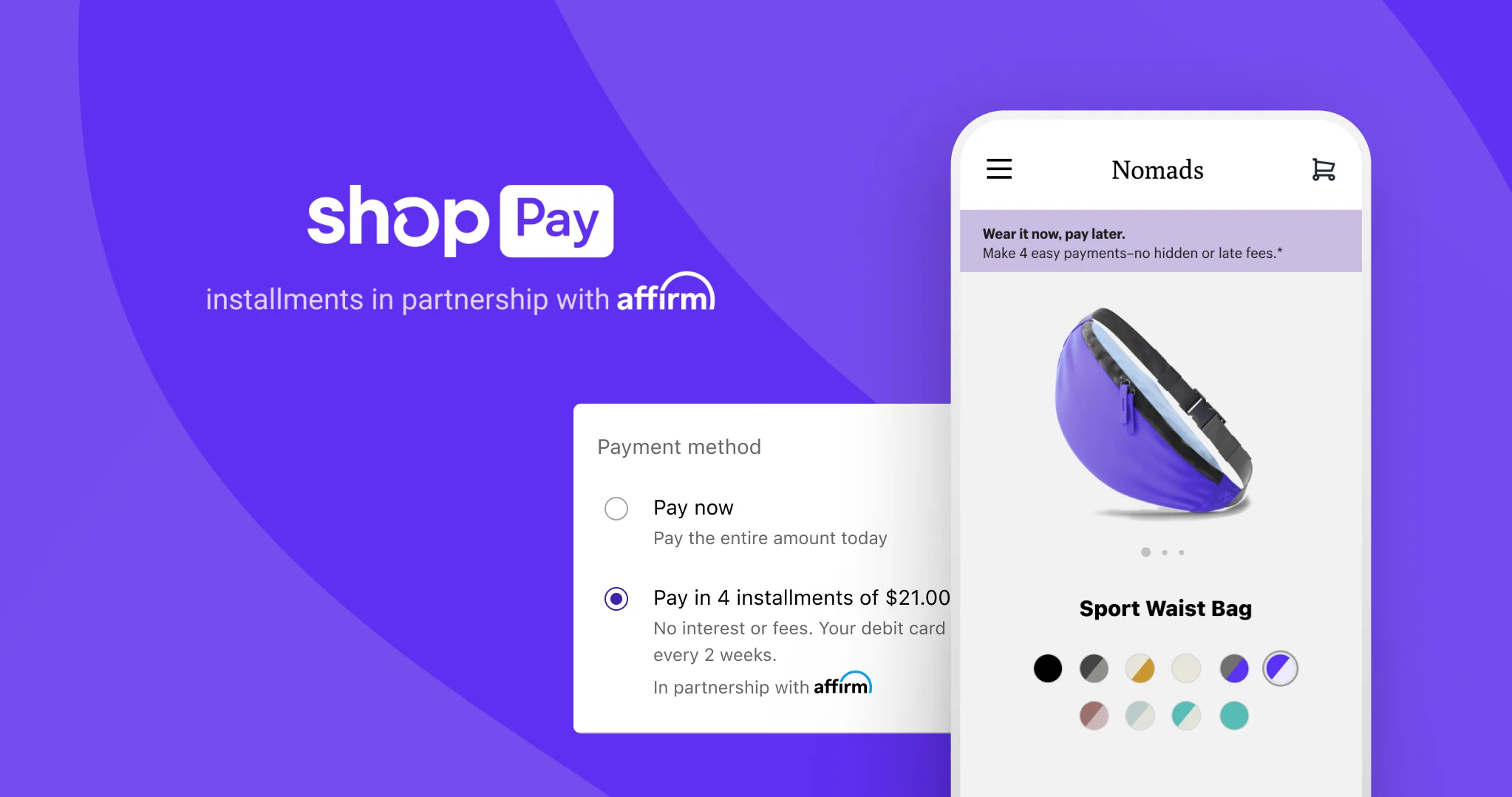

3. Shop Pay Installments

- Best For: All Shopify and Shopify Plus merchants

- Pricing: Included with Shopify Payments (no extra app cost)

- Payment Options: 4 interest-free payments or monthly financing

- Availability: UK, USA, Canada

Shop Pay Installments is Shopify's native BNPL solution, powered by Affirm. If you are already using Shopify Payments, Shop Pay Installments should be your first choice for one simple reason: it requires zero additional integration work and remains entirely within the native Shopify checkout environment. There is no redirect to a third-party site, no additional loading screens, and no friction points introduced by switching to an external provider's interface.

This frictionless experience delivers measurable conversion benefits. Merchants enabling Shop Pay Installments typically report 20-30% increases in conversion rates and 30-50% increases in average order value. The feature appears seamlessly within the payment method selector, positioned as a native part of the Shopify checkout experience. Customers choosing this option never leave your environment, which is psychologically powerful from a trust and conversion perspective.

The pricing is the strongest differentiator here. Because Shop Pay Installments is included with Shopify Payments, there is no incremental app fee. You pay the standard Shopify Payments transaction fees you are already paying, and the BNPL feature costs you nothing additional. For merchants already committed to Shopify Payments, this represents exceptional value and gives you a competitive advantage over smaller stores that may find third-party BNPL fees unaffordable.

Key features: Native integration, no app required, zero additional costs, integrated decisioning, no customer redirect, Shop Pay one-click checkout compatibility, detailed reporting, instant approval for most customers, compliance managed by Shopify.

Why choose them: If you are already on Shopify Payments, Shop Pay Installments is the obvious choice. The conversion metrics are the strongest in the industry because of the frictionless checkout experience. The pricing is unbeatable for established merchants already paying Shopify Payments fees. We recommend Shop Pay Installments as your primary BNPL option and a second provider (like Klarna or ClearPay) as a backup for customer choice.

4. PayPal Pay Later

- Best For: Stores already using PayPal checkout

- Pricing: Standard PayPal transaction rates apply

- Payment Options: Pay in 3 interest-free instalments (£30-£2,000)

- Availability: UK, USA, Australia, Germany, France, Spain, Italy

PayPal Pay Later represents an evolution of PayPal's offering, extending the power of the PayPal brand into the BNPL space. With over 400 million active PayPal accounts globally, the platform leverages existing customer trust and payment relationships to offer BNPL functionality without requiring new account creation or credit checks. For customers already logged into their PayPal account, enabling pay later is as simple as selecting it from their payment menu.

The simplicity of the PayPal ecosystem provides a unique advantage. Customers who already trust PayPal for their general spending are predisposed to trust PayPal Pay Later. This is particularly valuable for older demographic cohorts who may be hesitant about newer BNPL providers or unfamiliar with brands like Klarna or ClearPay. The buyer protection that PayPal is famous for extends to PayPal Pay Later transactions, providing an extra layer of customer confidence.

From a technical perspective, if you already accept PayPal checkout on your Shopify store, PayPal Pay Later appears automatically without requiring separate integration work. The £30 to £2,000 spending window is well-suited for mid-range purchases, though it does not handle very small impulse purchases or high-value luxury items. The lack of additional app fees makes PayPal Pay Later cost-effective for merchants already using PayPal.

Key features: Leverages existing PayPal accounts, no new credit checks, standard PayPal buyer protection, three equal interest-free payments, no separate integration required if using PayPal Checkout, broad geographic availability, competitive transaction rates.

Why choose them: If your customer base skews towards older demographics or PayPal users, PayPal Pay Later is a valuable addition to your payment options. The brand trust is exceptional, and the lack of technical implementation complexity is appealing. The combination with PayPal Checkout is particularly powerful for stores that already accept PayPal.

5. Laybuy

- Best For: Fashion and retail merchants in UK and NZ

- Pricing: Percentage-based merchant fee per transaction

- Payment Options: Pay in 6 weekly interest-free instalments

- Availability: UK, New Zealand

Laybuy is a New Zealand-founded BNPL provider that has built a strong presence in the UK market, particularly among fashion and retail merchants. What differentiates Laybuy from competitors offering pay-in-4 models is the six-weekly payment structure, which gives customers more breathing room between payments. For budget-conscious shoppers, spreading payments across six weeks rather than four fortnights can be the difference between abandoning a purchase and completing the transaction.

The Laybuy merchant platform includes sophisticated analytics and forecasting tools that help you understand BNPL adoption patterns and predict revenue impact. The Laybuy Boost marketing suite provides merchants with tools to promote BNPL options and reach new customers within the Laybuy ecosystem. Unlike some competitors, Laybuy provides detailed transaction-level reporting that integrates with your accounting systems, reducing manual reconciliation work.

The six-weekly model is particularly effective for mid-range purchases. For a £200 purchase, customers paying in six weekly instalments are only committing to £33-£34 per week, which feels more accessible than a £50 fortnightly payment. This psychological difference can drive meaningful conversion uplift in the fashion and lifestyle space where Laybuy has built its reputation.

Key features: Six weekly payments, Laybuy Boost marketing tools, detailed merchant analytics and forecasting, white-label checkout option, comprehensive reporting integration, customer rewards program, fast settlement.

Why choose them: If you operate a fashion or retail business selling mid-range items, Laybuy's six-weekly model is more customer-friendly than four-fortnightly alternatives. The marketing tools help you promote BNPL effectively, and the analytics provide insights into customer behaviour. The geographic focus on UK and NZ markets means the platform understands these specific markets deeply.

6. Splitit

- Best For: High-ticket Shopify stores

- Pricing: Per-transaction fee, no consumer fees

- Payment Options: Split payments using existing credit card

- Availability: UK, USA, Canada, Australia, Europe

Splitit represents a fundamentally different approach to BNPL. Rather than requiring customers to apply for credit or undergo a new financial product, Splitit splits charges across multiple transactions on a customer's existing credit card. This means customers need no new application, no credit check, and no additional accounts to manage. The approval is instantaneous because Splitit is simply dividing existing credit card transactions.

This model eliminates a major pain point of traditional BNPL. Customers can approve payments instantly without providing personal data, which is particularly valuable for privacy-conscious users and builds trust more quickly than competitors requiring formal applications. For merchants, this means no chargebacks related to payment failures or non-approval because the payment method already exists and has been verified by the customer's bank.

The lack of interest and fees for consumers is a significant differentiator. Customers are not taking on debt or paying interest to split their purchase. From a compliance and regulatory standpoint, Splitit sits outside traditional BNPL regulation because it is not technically credit. This has made Splitit popular with merchants wanting to offer flexibility without the growing regulatory overhead of traditional BNPL. Samsung and other premium brands have adopted Splitit, particularly for high-ticket electronics and luxury items.

Key features: No new credit applications, instant approval, no consumer interest or fees, uses existing credit cards, regulatory simplicity, white-label option, global availability, Samsung Wallet integration, fraud prevention included.

Why choose them: If you sell high-ticket items (electronics, furniture, luxury goods), Splitit removes barriers to conversion by making payment splitting frictionless. The elimination of credit checks means faster approvals and more satisfied customers. The lack of regulatory complexity is increasingly valuable as UK BNPL regulation tightens.

7. Affirm

- Best For: High-value purchases on Shopify

- Pricing: Merchant fees vary by plan

- Payment Options: Monthly instalments from 4 payments to 60 months, 0-36% APR

- Availability: USA, Canada, expanding UK

Affirm is the largest pure-play BNPL provider globally and the technology behind Shop Pay Installments. In addition to powering Shopify's native BNPL, Affirm is available as a standalone integration for merchants wanting access to Affirm's broader financing options. The key strength of Affirm is the range of financing terms available, from short-term pay-in-4 up to 60-month financing plans at various APR levels.

Affirm's decisioning engine is sophisticated, offering different terms and APR to different customers based on their creditworthiness. For high-value purchases like furniture, appliances, or luxury goods, this ability to offer longer-term financing (up to 60 months) or variable APR is transformative. A customer might be able to finance a £3,000 sofa over 36 months at a reasonable APR, whereas traditional BNPL providers cap out at £500 or £1,000 limits.

The UK expansion is gaining pace, with Affirm increasingly available to UK merchants. If you are selling high-ticket items, Affirm's presence as both the Shop Pay backend and a standalone option gives you flexibility. The real-time decisioning means customers see exactly what terms they qualify for before committing to purchase, reducing surprises and chargebacks.

Key features: 60-month financing options, variable APR terms, real-time decisioning, white-label option, merchant dashboard with insights, fraud protection, highest spending limits in BNPL industry, Shop Pay integration.

Why choose them: If you sell high-value items or want to offer longer-term financing options, Affirm is the gold standard. The flexibility to offer everything from four-payment plans to five-year finance at various APRs means you can serve a wider range of customer financial situations. Affirm's expanding UK presence makes now the time to explore integration.

8. Sezzle

- Best For: Budget-conscious Gen Z shoppers

- Pricing: 6% + £0.30 per transaction

- Payment Options: 4 interest-free fortnightly payments

- Availability: USA, Canada, growing UK presence

Sezzle has positioned itself as the responsible BNPL provider, emphasising customer financial health and literacy. The platform includes Sezzle Up, a feature that helps customers build credit scores while using BNPL services. This appeals particularly to younger customers who are early in their credit journeys and value the opportunity to demonstrate creditworthiness alongside accessing immediate purchasing power.

The transparent fee structure (6% plus 30p per transaction) is straightforward for merchants to budget. Sezzle does not include hidden charges or variable fees that fluctuate based on customer behaviour. For merchants operating on thin margins, this predictability is valuable. The platform also offers payment rescheduling functionality, allowing customers to adjust payment dates if they face temporary financial hardship, which reduces missed payments and chargebacks.

Sezzle's backend analytics are robust, giving merchants insights into customer behaviour, repeat purchase rates, and BNPL adoption patterns. The platform is growing in the UK market and is a solid alternative to the more established Klarna and ClearPay if you want to differentiate your offering or reach customer segments prioritising financial responsibility.

Key features: Sezzle Up credit-building feature, flexible payment rescheduling, transparent fee structure, comprehensive merchant analytics, customer education focused, responsible lending messaging, mid-size transaction focus.

Why choose them: If your audience values financial responsibility and you want to position BNPL as part of a customer's credit-building journey, Sezzle is distinct. The clear fee structure and rescheduling functionality reduce the risk of missed payments. Growing UK presence makes this a good time to explore partnership.

9. Scalapay

- Best For: European-focused Shopify merchants

- Pricing: Percentage per transaction

- Payment Options: Pay in 3 or 4 interest-free instalments

- Availability: UK, Italy, France, Germany, Spain, Portugal, Finland, Belgium, Netherlands

Scalapay is an Italian-founded BNPL provider expanding rapidly across Europe and into the UK. The platform specialises in cross-border commerce, making it exceptionally valuable for Shopify merchants selling across multiple European markets. If you ship to customers in Germany, France, or Spain, Scalapay enables you to offer BNPL in local currencies and languages, dramatically reducing friction for international customers.

The three-or-four payment model is flexible, allowing customers to choose whether they prefer three payments or four fortnightly instalments. This flexibility appeals to customers with different cash-flow patterns. Scalapay's merchant dashboard includes detailed reporting on international sales, cross-border payment patterns, and success rates by geography, helping you optimise your European expansion strategy.

While Scalapay has lower brand recognition in the UK than Klarna or ClearPay, the platform is growing quickly and has secured significant investment and partnerships. For fashion and lifestyle brands with European ambitions, Scalapay solves a real problem that other UK-focused BNPL providers do not address. The platform's multilingual and multi-currency support is genuinely sophisticated.

Key features: Multi-currency support, broad European coverage, flexible three-or-four payment options, international merchant dashboard, white-label option, fast settlement, local payment method integration by country.

Why choose them: If you sell to European customers or have ambitions to expand across Europe, Scalapay is invaluable. The local currency and language support removes friction for international customers. For UK merchants expanding into Europe, Scalapay is more suited than UK-only providers.

10. DivideBuy

- Best For: Furniture, electronics, and high-value UK retailers

- Pricing: Variable based on finance terms

- Payment Options: Interest-free and interest-bearing finance, up to 12 months

- Availability: UK only

DivideBuy represents a different category within the BNPL space. Whilst most BNPL providers focus on short-term interest-free payments, DivideBuy is an FCA-regulated point-of-sale finance provider that offers both interest-free and interest-bearing finance for terms up to 12 months. This positions DivideBuy perfectly for furniture, electronics, and other high-value items where customers genuinely need longer-term finance to afford the purchase.

The key strength of DivideBuy is the ability to offer true point-of-sale finance embedded directly into your Shopify checkout. Customers see finance options at the exact moment they are making a purchase decision, and the integration with DivideBuy's decisioning engine means approvals happen in seconds. For merchants selling sofas, garden furniture, or high-end electronics, this bridge between instant BNPL and longer-term consumer finance is powerful.

The FCA regulation means DivideBuy must follow strict affordability and responsible lending practices. For customers, this translates to peace of mind that the finance product is properly regulated. For merchants, it means lower risk of regulatory issues as BNPL regulation tightens. The 12-month term option handles purchase price points that traditional BNPL cannot accommodate.

Key features: 12-month finance terms, interest-bearing and interest-free options, FCA-regulated, white-label checkout, instant customer decisioning, UK specialist, point-of-sale finance integration, comprehensive compliance management.

Why choose them: If you sell furniture, home improvement products, or high-ticket electronics, DivideBuy's 12-month finance terms are superior to any BNPL alternative. The FCA regulation provides regulatory clarity that other BNPL providers lack. The specialist UK focus means the product is designed precisely for the UK market.

What Is Buy Now Pay Later?

Buy now pay later is a payment method that allows customers to make purchases immediately and pay for those purchases over a series of instalments, typically without interest. Unlike traditional credit products that require credit checks and formal applications, BNPL products emphasise speed and simplicity. A customer can be approved for BNPL in seconds using just an email address and basic identity information.

From a merchant perspective, BNPL works by the provider paying the merchant the full order value immediately (or within one business day), and then collecting payments from the customer in instalments. The merchant gets paid upfront, the customer gets flexible payment, and the BNPL provider assumes the credit risk. The merchant pays a fee, typically between 2% and 8% per transaction, for this service.

BNPL has evolved to include two distinct models. Transparent BNPL (interest-free models from Klarna, ClearPay, and others) appeal to customers who want flexibility without cost. Finance BNPL (from providers like Affirm and DivideBuy) offers longer-term options with variable interest rates, serving customers making larger purchases who need more affordable monthly payments. Both models are valuable depending on your product category and price points.

Benefits of Buy Now Pay Later for Shopify Merchants

The primary benefit of BNPL for merchants is an immediate uplift in conversion rates. Customers frequently abandon shopping carts because the total price feels unaffordable at the moment of purchase. BNPL removes this barrier by allowing customers to spread payments across weeks or months. The psychological impact of "four payments of £50" feeling more affordable than a single £200 charge is well-documented and powerful.

The secondary benefit is increased average order value. When customers know they can pay in instalments, they are more willing to purchase higher-value items or add additional products to their basket. Merchants consistently report AOV increases of 30-50% after enabling BNPL. For a store generating £100,000 monthly in sales, a 40% AOV increase represents £40,000 in additional monthly revenue before considering the BNPL fees.

BNPL also attracts younger customer demographics. Customers aged 18-35 have higher BNPL adoption rates than older cohorts, and enabling BNPL on your store signals that you understand modern purchasing preferences. This is particularly valuable for fashion, beauty, and lifestyle brands where younger customers represent significant market share.

The final major benefit is competitive advantage. If your competitors do not offer BNPL and you do, you capture customers that would otherwise shop elsewhere. Conversely, if your competitors offer BNPL and you do not, you lose customers at checkout who specifically search for BNPL options. BNPL has become so common that not offering it increasingly feels like a competitive disadvantage rather than a differentiating feature.

How to Choose the Right BNPL App for Your Shopify Store

The most important factor in choosing BNPL is understanding your customer demographics. If your core audience is Gen Z and millennials, ClearPay is likely to outperform alternatives because your customers are already familiar with the brand. If your audience skews older, Klarna or PayPal Pay Later might resonate more strongly. If you are unsure, Klarna is the safest choice because it has the highest brand recognition across age groups in the UK.

The second factor is your average order value. If your typical order is under £100, simple four-payment BNPL solutions (Klarna, ClearPay, Shop Pay Installments) work well. If your average order is £500 or above, you need a provider like Affirm or Splitit that handles higher values. If you sell furniture or electronics with orders regularly exceeding £2,000, DivideBuy's longer-term financing is essential.

Merchant fees should factor into your decision, but do not make it the primary consideration. A provider charging 6% but delivering a 40% conversion uplift is vastly superior to a provider charging 3% but delivering no uplift. Run the mathematics: if adding BNPL increases your conversion rate by 25% with a 3% fee, is that better or worse than your current situation? In nearly all cases, the conversion uplift more than offsets the fee.

Integration complexity matters less for Shopify merchants than for other platforms because Shopify provides native apps for all major BNPL providers. However, Shop Pay Installments requires literally zero integration work if you are already on Shopify Payments, making it the easiest option. If you want multiple BNPL providers, consider how many separate integrations your team can manage and support.

Finally, consider your specific product category. Fashion brands benefit most from Klarna and ClearPay. High-ticket sellers need Affirm or Splitit. Furniture retailers need DivideBuy. European merchants need Scalapay. Rather than trying to optimise for every possible BNPL provider, choose one or two that match your specific business model and customer base.

How BNPL Affects Shopify Checkout Conversion

BNPL increases conversion by solving the most common reason customers abandon shopping carts: sticker shock at the total payment amount. When a customer sees a £300 total and realises they need to pay the entire amount immediately, many will leave the store. When that same customer sees "four payments of £75", the purchase feels far more accessible and the abandonment risk drops significantly.

The visibility of BNPL options within your checkout is critical. For Shop Pay Installments, the option appears natively within the payment method selector, making it prominent without being intrusive. For external BNPL providers, the visibility depends on how prominently you display their payment buttons and messaging. Many merchants find that adding simple messaging like "or split into 4 payments" above the add-to-cart button has measurable impact on conversion even before checkout.

BNPL also functions as a trust signal. When customers see that your store accepts Klarna or other reputable BNPL providers, it signals that you are a legitimate, established business. The presence of multiple payment options including BNPL is subconsciously interpreted as a signal of trust. This is particularly powerful for new stores or brands that customers are less familiar with.

The data shows that customers specifically searching for BNPL options have higher intent and lower bounce rates. These customers are actively selecting BNPL at the payment stage, meaning they have already decided to purchase and simply want to split the payment. Supporting BNPL means you capture these high-intent customers that alternative payment methods might miss.

Buy Now Pay Later Trends for 2026

Regulation is reshaping BNPL in 2026. The FCA's regulation of BNPL lending in the UK has introduced affordability requirements and responsible lending practices that traditional BNPL providers must now follow. This means slower approval decisions for some providers and more stringent verification for others. However, it also means customers have greater protections, which increases trust in BNPL products overall.

AI-powered credit decisions are becoming increasingly sophisticated. Providers are using machine learning to make real-time decisioning based on hundreds of data points, not just credit score and income. This means approval rates are improving even as lending becomes more responsible. Customers are being approved faster with more nuanced underwriting that reduces both chargebacks and over-lending.

B2B BNPL is emerging as a significant growth area. Whilst this article focuses on consumer-facing Shopify stores, many BNPL providers are expanding to support Shopify Plus merchants selling to other businesses. The ability to offer BNPL to business customers is opening new market opportunities.

BNPL in subscription commerce is gaining traction. More subscription box services and membership-based Shopify stores are integrating BNPL to allow customers to split their subscription costs across instalments. This is particularly valuable for premium subscriptions where the monthly cost is high.

Integration with Shopify's checkout extensibility API is becoming the standard. Rather than BNPL providers building custom integrations, they are leveraging Shopify's native extensibility framework to provide seamless experiences that require minimal merchant configuration. This makes BNPL integration simpler and more reliable for Shopify merchants.

Risks and Considerations for Shopify Merchants

Merchant fees can erode margins if you do not plan carefully. A BNPL fee of 5-6% on a product with a 20% gross margin is consuming 25-30% of your profit. Before implementing BNPL, calculate whether the conversion uplift justifies the fee impact. In most cases it does, but for low-margin products or mature categories, BNPL fees can be problematic.

Chargebacks and disputed transactions remain a risk despite BNPL providers' fraud prevention. If a customer claims they did not make a purchase or disputes a charge, the BNPL provider may reverse the payment, leaving you without both the product and the payment. Fraud prevention is improving but represents an ongoing risk compared to cash-in-hand transactions.

Consumer over-spending is a valid concern that regulators and responsible lenders are working to address. When a customer can split any purchase into instalments, the temptation to buy beyond their means increases. Responsible BNPL providers like Sezzle and regulated providers like DivideBuy implement safeguards to prevent over-lending, but this remains an area of societal concern that may lead to further regulation.

Regulatory changes in the UK and Europe continue to evolve. What is allowed today may be restricted tomorrow. The FCA's regulation of BNPL is still developing, and additional restrictions on lending or merchant fees could impact your ability to use BNPL effectively. Stay informed about regulatory developments affecting BNPL in your markets.

Too many BNPL options can create decision fatigue at checkout. If you offer five different BNPL providers, customers may spend excessive time comparing options rather than completing purchase. We typically recommend two to three BNPL providers maximum. Choose one or two primary options and potentially one backup alternative.